Where Serious Difficulty Really Lays

It is the details of such plans as well as implementation strategies where the difficulty will lay. Groups like Richemont are not known for agility or being able to make decisions quickly. If anything, Richemont has moved to decrease the decision-making ability of its managers to an environment where permission to make decisions must in many instances be granted by the board or committees. Thus, even though Richemont appears to know what its future must look like, it is unclear how it will achieve these goals by making broad sweeping decisions from a committee or board level, and not giving individual brands or managers the ability to make decisions that are correct for their specific brands, their teams, their products, and their markets.

In our opinion, Richemont would be well-advised to consider offering broad policy and operational changes while allowing talented managers and teams to operate relatively freely in managing their brands and tasks. In many ways, many of the employees of Richemont are in a sort of holding pattern while having to wait for the Group in general to decide what it wants to do. This might very well be a situation that leads to excessive waste at a time when changes need to happen a bit faster. At the same time, it is equally likely that the current business environment and deployed strategies are so unsustainable (as Richemont refers to it) that the best thing to do is literally reform the Group’s production, distribution, and marketing strategies from the ground up and prevent further major business activity until a better operating environment has been established at the Group and its brands.

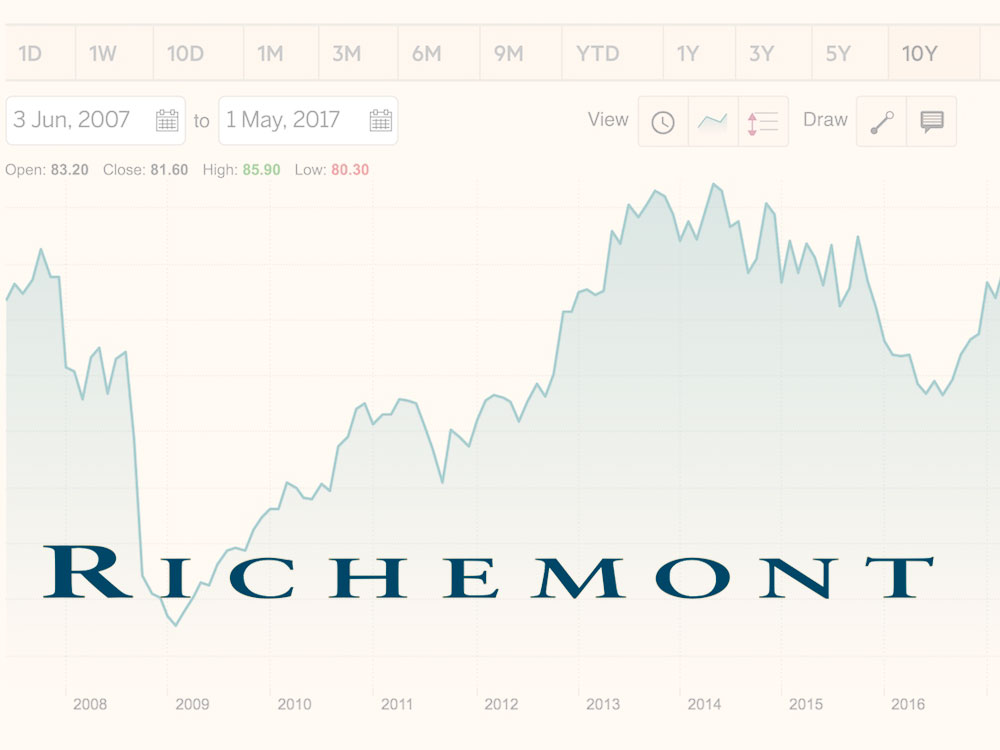

From a cash perspective, Richemont is in an excellent position, reporting a net cash position of 5.79 billion euros. The group has billions of dollars in cash, despite extensive share buy-back programs. This means that even if the group is losing money, they still have plenty of it in reserves to keep going for many years. With that said, no group wants to endure losses for too many periods in a row, which is why Richemont and its colleagues are starting to get very serious about rebuilding their businesses to operate successfully in our modern era.

At the end of the day, Richemont has some very smart people running its key groups and is now directly facing – perhaps a bit too long after it should have – the fact that the traditional business of luxury watches has irreversibly changed after the internet decimated traditional distribution and sales, and have fundamentally changed marketing strategies.

The luxury watch industry, an industry so prone to focusing on tradition and routine, has been experiencing extreme highs and lows over the last two decades. Many highs and lows which it was loath to or, frankly, simply ill-equipped to properly handle. It does appear that the industry is now very serious about effectuating more than mere band-aid solutions to its most serious problems. Solutions that with any luck and some aggressive decision-making, will lead to the reformation of business practices, and an environment where growth and development can actually happen.

Richemont Headquarters, Geneva, Switzerland

What we are seeing is a company keenly concerned about creating efficiencies and trying to shift its business practices to eventual recovery – still, recovery is going to be a long and very difficult practice for the watch industry and Richemont.

It is important to also note that the watch industry itself isn’t going to go away. Rather, we liken the current situation to the industry having a disease – several of them, in fact. Assuming the industry successfully cures those diseases, such as over-production of inventory, lack of marketing performance, and short-sighted commercial endeavors, the watch industry should first hit a baseline performance plateau as things stop dropping. It will then be able build itself back up from there taking into consideration modern business practices in a digital, connected world where distribution and marketing practices must be wholly rethought. richemont.com