The Swiss watch industry was likely hoping for some performance rebounds at the end of 2016 in anticipation of the holiday shopping season, but alas such hopes have not been realized. Rather than proclaim “doom and gloom,” I prefer to see this as part of a larger trend of returning to normalcy. Swiss watch exports are, in my opinion, returning to sustainable levels that they perhaps should be at without the existence of bubble markets or inflated economies.

Still, the numbers don’t bode well for shareholders and growth-seekers, of which there are many in today’s watch industry. Let’s examine some of the October 2016, and recently released November 2016 Swiss watch export numbers as published by the Federation of the Swiss Watch Industry (FH, for short). They also released an accompanying summary sheet which attempts to put additional metrics into context, and sums up more of what we are looking at. My aim, in addition to commenting on some of the broader items, is to also discuss what the top markets for Swiss watch exports (and more than likely end-consumer sales) are at the end of 2016.

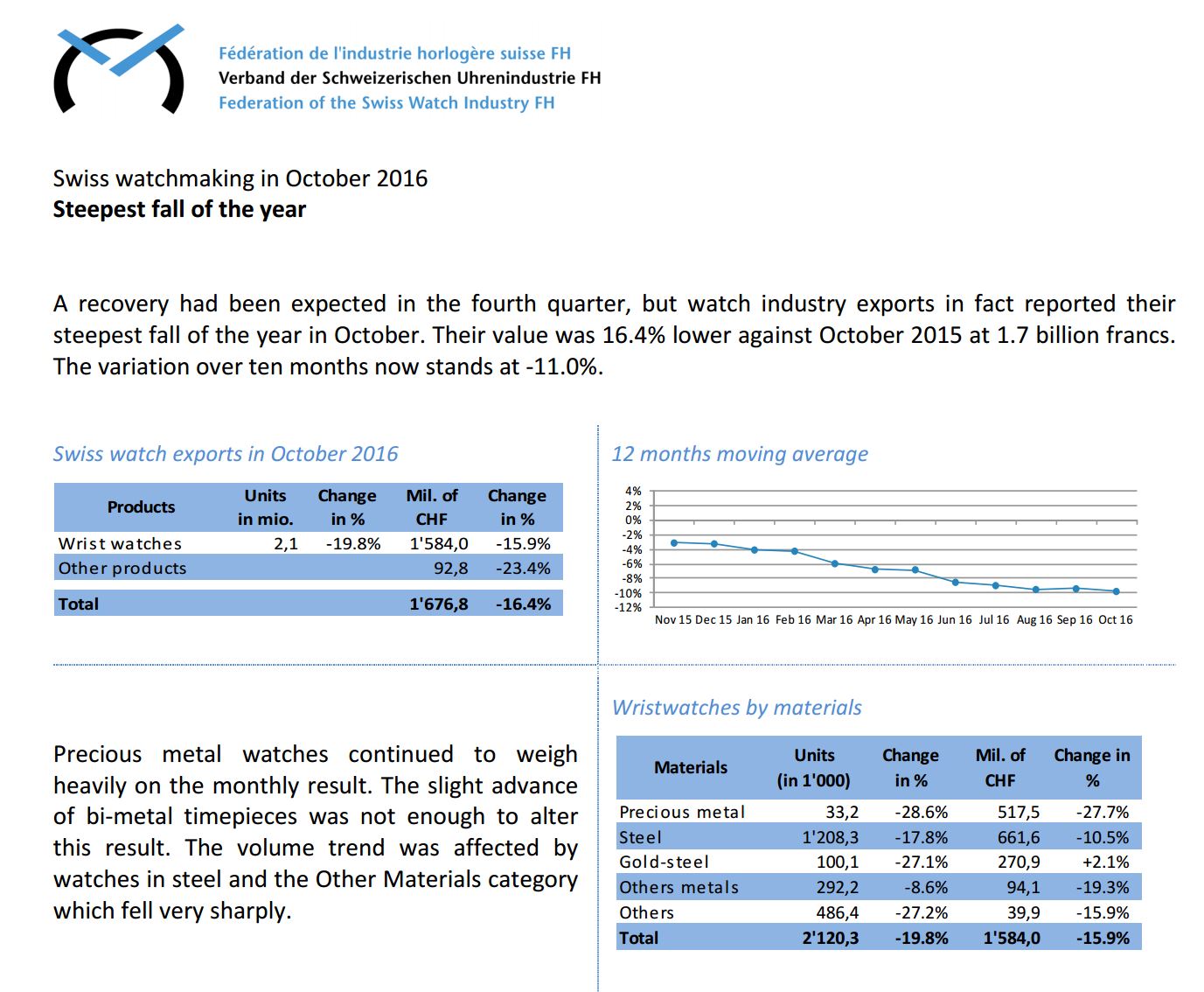

Summary of Swiss Wristwatch Exports in October, 2016. Source: fhs.swiss

“Steepest fall of the year” reads the headline of the October 2016 report. The FH even goes on to say that they had been expecting a recovery for the fourth quarter of the year while, by stark contrast, the Swiss watch industry actually reported its steepest fall of 2016 in October. They say export value against October 2015 has fallen to 1.7 billion Swiss francs, but that includes about 90 million Swiss francs in “other products,” so the overall export value was 1.584 billion Swiss francs.

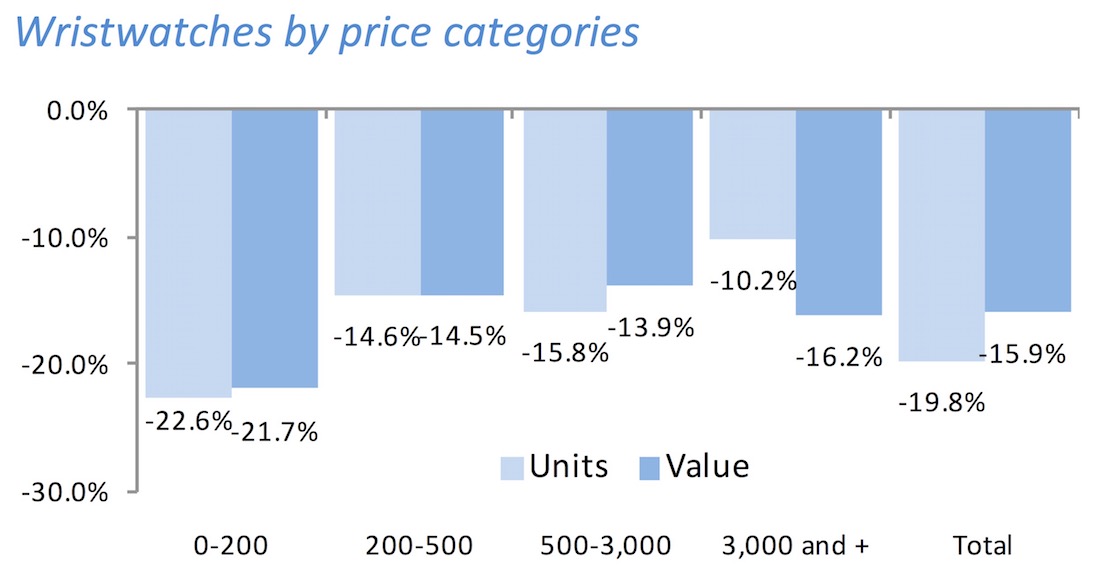

Swiss Wristwatch Export By Price Categories in October, 2016. Source: fhs.swiss

This chart, above, clearly doesn’t look pretty. Compared to the same period in 2015, shipped units dropped between 22.6% and 10.2%, while export value dropped by somewhere between 14.5% and 21.7%. What I want to make clear up front is that the major decreases in exports of watches represented what we would refer to as inexpensive watches. Watches valued at under 200 Swiss francs were down almost 23% in volume, compared to about a 16% reduction in watches valued at over 3,000 Swiss francs. This was for October 2016, and it is important to realize that overall exports for 2016 are 16.4% down from the year before and down 11% for 2016 overall. That is certainly enough for heavily impacting a lot of balance sheets.

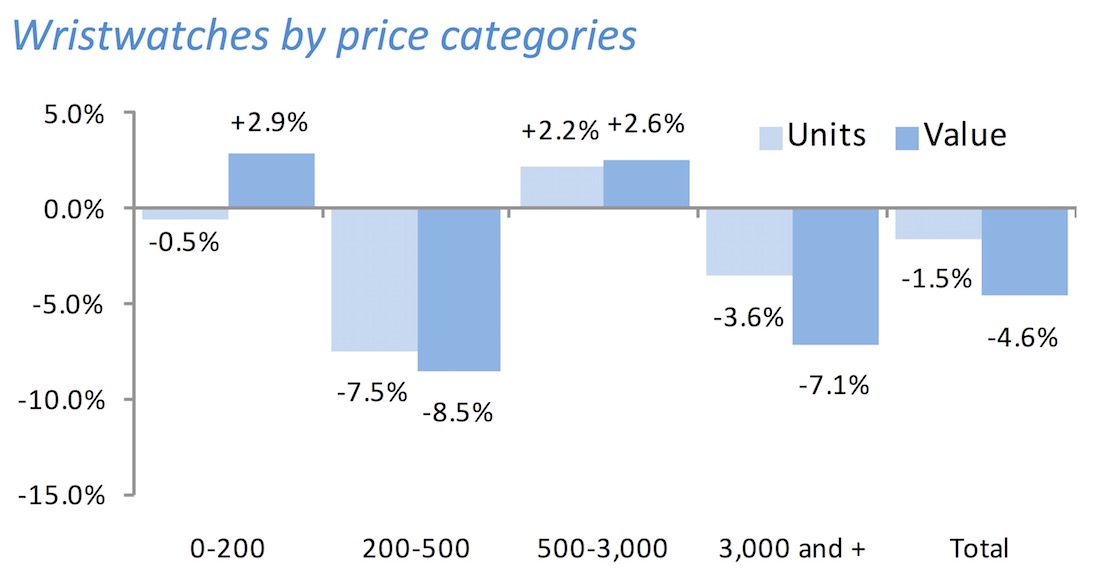

Swiss Wristwatch Export By Price Categories in November, 2016. Source: fhs.ch

Things began to flatten out in November with some minor growth areas here and there, and yet continued steep declines in the 200-500 and 3,000+ Swiss francs segments. The cheapest segment (ruled by Swatch) recovered and so did the 500-3,000 Swiss francs segment, clearly indicating the prevailing appeal and potential that the latter, “mid-level luxury” watches have.

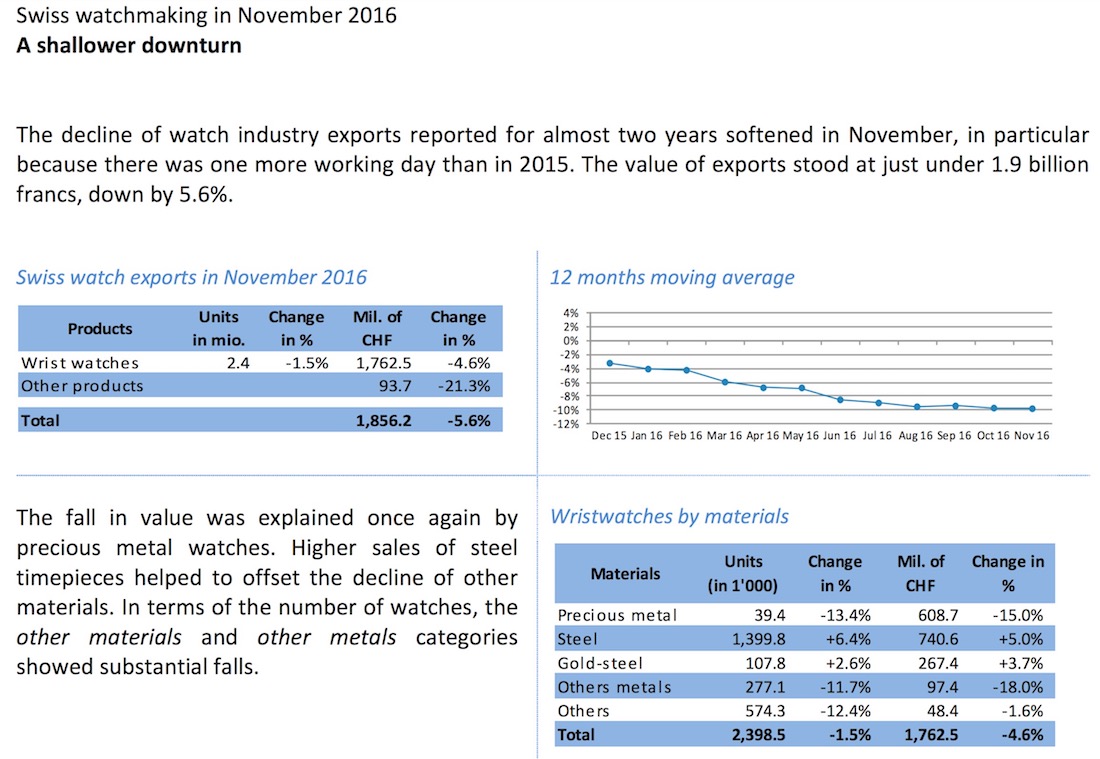

Summary of Swiss Wristwatch Exports in November, 2016. Source: fhs.swiss

As a general trend, we can say that export value decreased more than volume which essentially means that prices are going down. I’ve been saying for years that watch prices are too high (and they don’t need to be), so it is good to see signs that prices are going down. Brands have been talking about this, but it is important to see overall price points decreasing, even in the high-end segments.

This noted, we have to bear in mind that such a rationalization doesn’t mean people don’t want nice things. The only gain in exports value in disastrous October was in two-tone (i.e. gold and steel) watches which experienced a 2.3% increase in exports. Compare that to a 27.7% decrease in all-gold watches. As for November, steel watches joined two-tone watches and gained a few percentage points. Again, consumers want value, and retailers are responding in terms of what they are ordering.